This section of the guidance provides details on the application of the Scottish Aggregates Tax for aggregate that has been supplied by a business located elsewhere in the UK, i.e. England, Wales or Northern Ireland (rest of the UK) to a customer in Scotland. For ease ‘rest of the UK’ has been abbreviated to rUK, throughout this section)

HMRC has published cross border guidance that provides details on the application of the UK Aggregates Levy for aggregate that has been supplied by a business located in Scotland to a customer based in the re UK .

If you are a Scottish based supplier who is supplying aggregate to a customer in rUK then a Scottish Aggregates Tax credit may be available to you.

If you have any uncertainty about how Scottish Aggregates Tax should be applied, then please contact SAT@revenue.scot.

Contents

- Introduction

- Scottish commercial exploitation

- Aggregate moving from rUK to Scotland – Direct transfers

- Aggregate moving from the rUK to Scotland – Indirect transfers

- Other scenarios

Introduction

Scottish Aggregates Tax will replace the UK Aggregates Levy in Scotland as from 1 April 2026. The UK Aggregates Levy was introduced in 2002 for all UK nations and there will be similarities to the way that the Scottish Aggregates Tax and the UK Aggregates Levy operate as taxes. Up until 31 March 2026 the UK Aggregates Levy will be chargeable on all aggregate that is subjected to commercial exploitation (unless the aggregate is exempt).

Scottish Aggregates Tax will be charged on any occasion where aggregate is subjected to commercial exploitation in Scotland (unless the aggregate is exempt).

UK Aggregates Levy will remain chargeable for commercial exploitation in other UK nations (England, Northern Ireland and Wales). This means that where there is movement of aggregate from Scotland to anywhere else in the UK or from anywhere else in the UK to Scotland there will be two different aggregate taxes that may apply.

HMRC and Revenue Scotland have worked together in establishing rules to manage cross border transactions and avoid double taxation (i.e. both UK Aggregates Levy and Scottish Aggregates Tax being charged on the same transaction). The following guidance gives details on when aggregate will be chargeable to Scottish Aggregates Tax in cross border transactions, where a rest of the UK based business supplies aggregate to a Scottish based customer.

HMRC’s guidance on cross border transactions gives details on when aggregate would be chargeable to the UK Aggregates Levy in cross border transactions, where a Scottish based business supplies aggregate to a rest of the UK based customer.

Scottish commercial exploitation

Scottish Aggregates Tax will be charged on aggregate that has been commercially exploited in Scotland (unless the aggregate is exempt). Scottish based commercial exploitation is taken to occur in two ways.

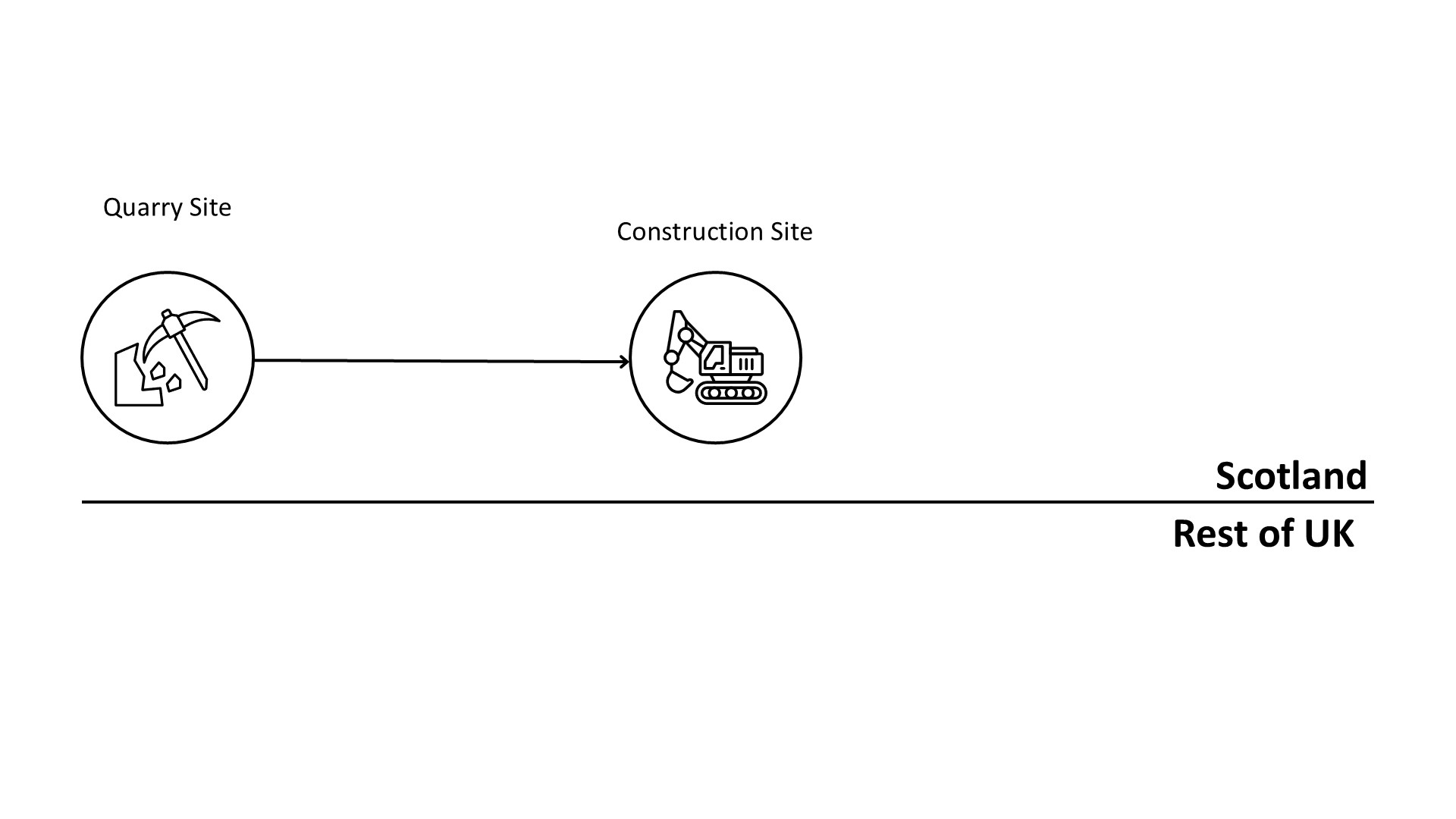

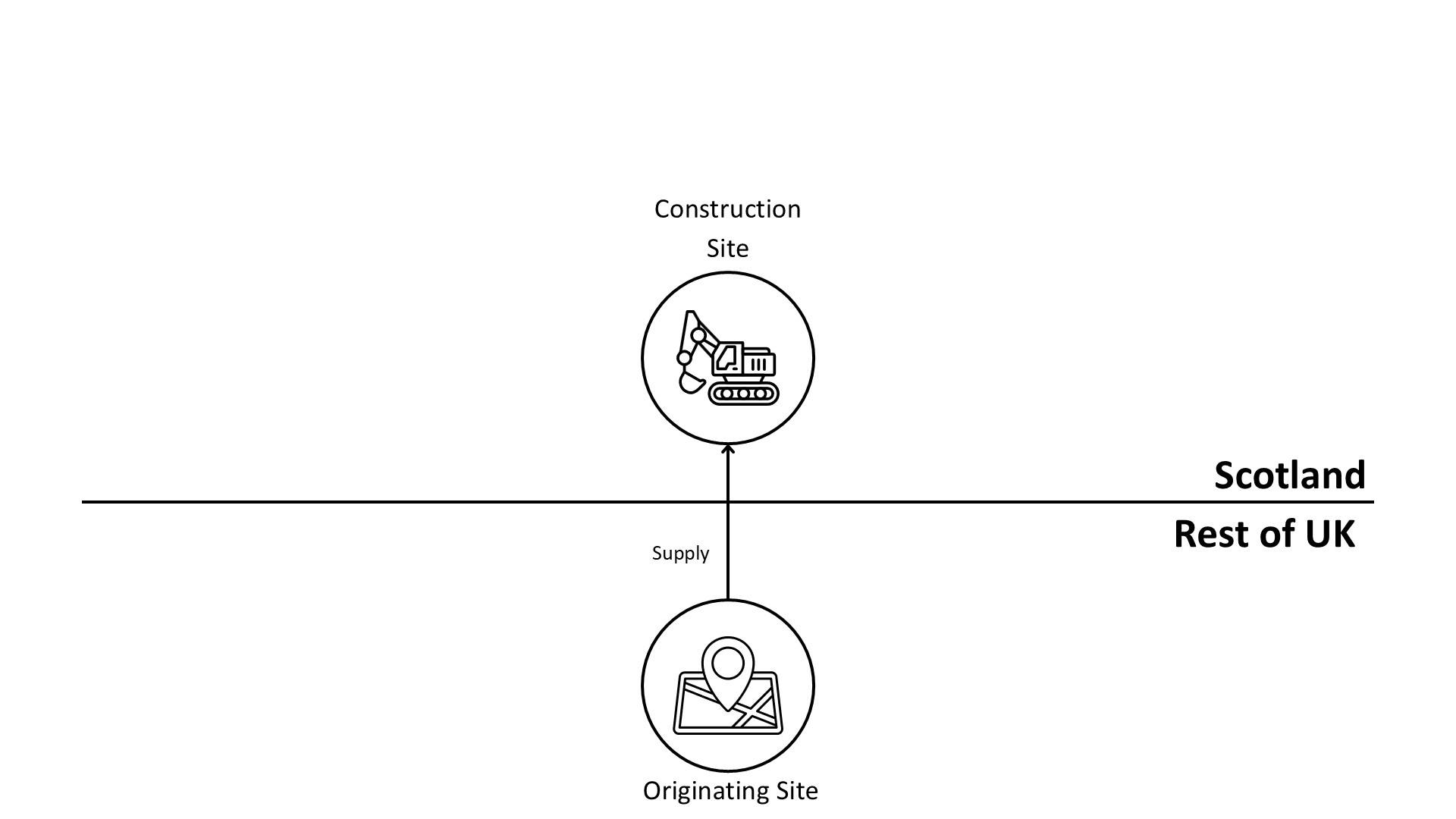

The first way is when the aggregate is in Scotland at the time when it is subjected to exploitation. For example, if aggregate is sold from a Scottish quarry to a construction firm (whether that firm is based in Scotland or rUK) the commercial exploitation will be taken to have occurred in Scotland.

Diagram 1 – direct supply from a Scottish site to a Scottish customer

The second is where a quantity of aggregate has been subjected to exploitation by either:

- it being removed from a site, or

- being part of an agreement to supply

and this exploitation has occurred as a result of the aggregate being moved to Scotland from the rUK (including rUK waters).

For example, if a quarry site based in England sells and delivers aggregate to a Scottish customer, then this transaction will be considered Scottish commercial exploitation for the purposes of the Scottish Aggregates Tax.

This guidance focuses on this second type of ‘cross border’ commercial exploitation.

Aggregate moving from rUK to Scotland – Direct transfers

This guidance describes aggregate that moves from an rUK based supplier to a Scottish customer, without any intermediary in the supply chain, as a ‘direct transfer’. There are more complicated transactions involving multiple persons in the supply chain, those are described as ‘indirect transfers’.

If Scottish commercial exploitation occurs due to movement of aggregate from an rUK supplier to a Scottish based customer, then Scottish Aggregates Tax will be due on that transaction (unless any relevant exemption applies). The rUK supplier will be required to register with Revenue Scotland for Scottish Aggregates Tax and pay any tax due, regardless of whether that business has any presence in Scotland. The Scottish customer will consequently be exempt from Scottish Aggregates Tax in respect of that supply as the aggregate has already been subjected to Scottish Aggregates Tax.

The rUK supplier will also be required to register with HMRC for the UK Aggregates Levy (if they are not already registered) but will be able to a claim for a UK Aggregates Levy tax credit for this transaction provided they hold evidence that the aggregate has crossed the border from rUK to Scotland. Further guidance on this type of claim can be found in HMRC's guidance.

If you have any uncertainty about how Scottish Aggregates Tax should be applied, then please contact SAT@revenue.scot.

If you have any uncertainty about how the UK Aggregates Levy should be applied, then please contact enquiries.eeitts@hmrc.gov.uk.

A quarry site based in rUK sells and delivers aggregate to a Scottish based construction firm.

Diagram 2 - direct supply from rUK to Scotland

The rUK quarry operator will be required to:

- register with Revenue Scotland and register with HMRC if they have not already done so

- make a return to HMRC which includes a claim for a UK Aggregates Levy tax credit in relation to the supply of aggregate

- make a return to Revenue Scotland detailing the Scottish Aggregates Tax due in relation to the aggregate (making an SAT return)

The Scottish customer will not be required to register as a Scottish Aggregates Tax taxpayer or pay Scottish Aggregates Tax in respect of these supplies.

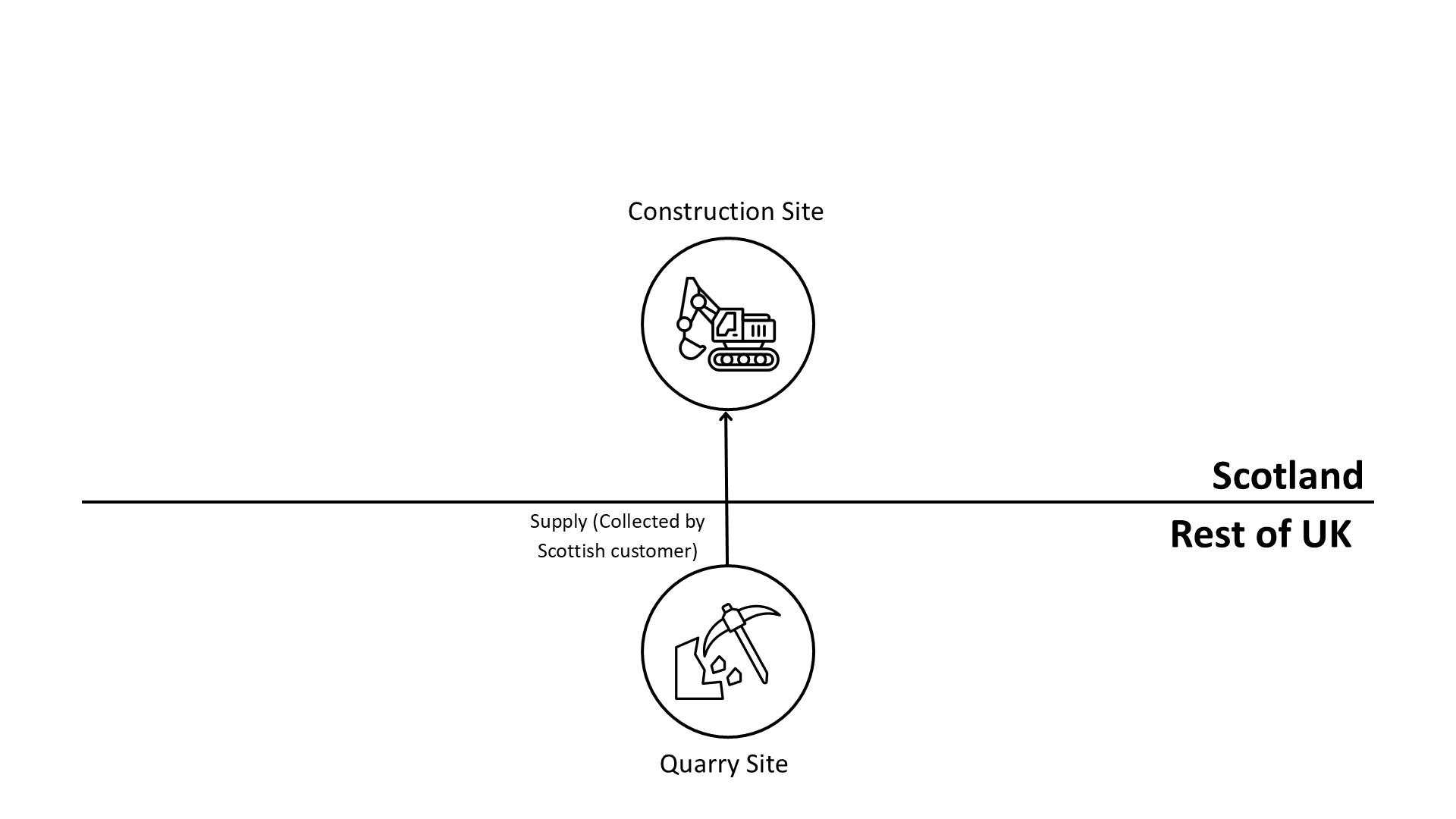

A Scottish based customer collects aggregate from an rUK based quarry for use on a construction project in Scotland.

Diagram 3 - collection by a Scottish customer from an rUK site

The rUK quarry operator will be required to:

- register with Revenue Scotland and register with HMRC if they have not already done so

- make a return to HMRC which includes a claim for a UK Aggregates Levy tax credit in relation to the supply of aggregate

- make a return to Revenue Scotland detailing the Scottish Aggregates Tax due in relation to the aggregate

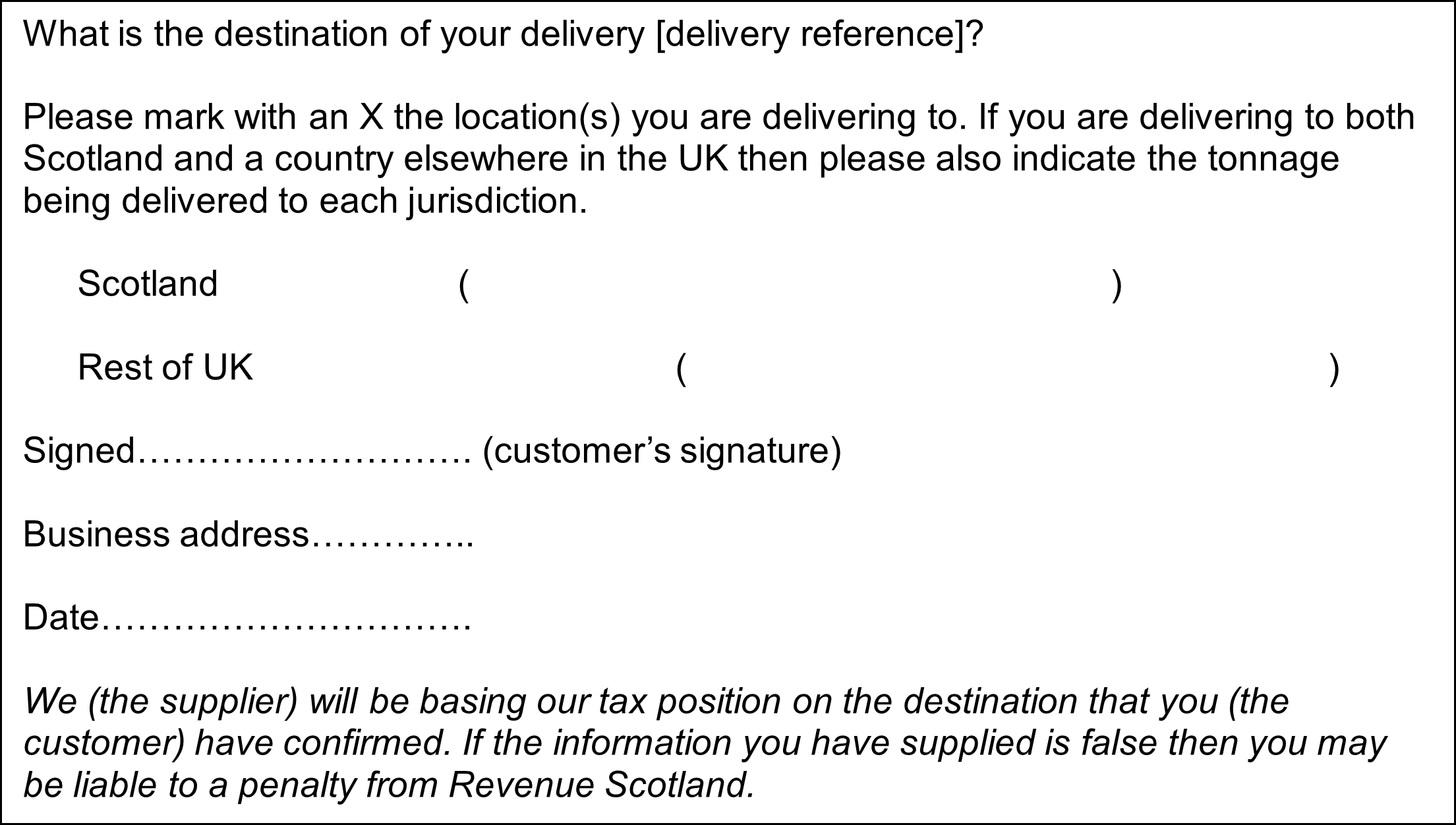

The quarry operator is also required to determine whether a customer who collects aggregate from a site is delivering that aggregate to Scotland or somewhere else in the UK. Records must be kept by the quarry operator that detail the destination of aggregate being collected (see below for an example record template). These records must detail:

- the delivery reference

- the destination of the aggregate (Scotland or rUK)

- a signature from the customer

- the customer’s business address

- a statement from the supplier that sets out the relevance of the declaration being made by the customer and the potential consequence for the customer if the declaration is made falsely

If a customer provides a false statement, then they may be chargeable to a penalty of 100% of the potential lost Scottish Aggregates Tax revenue in relation to the delivery being made. Please see RSTP3012 for further details.

Example record

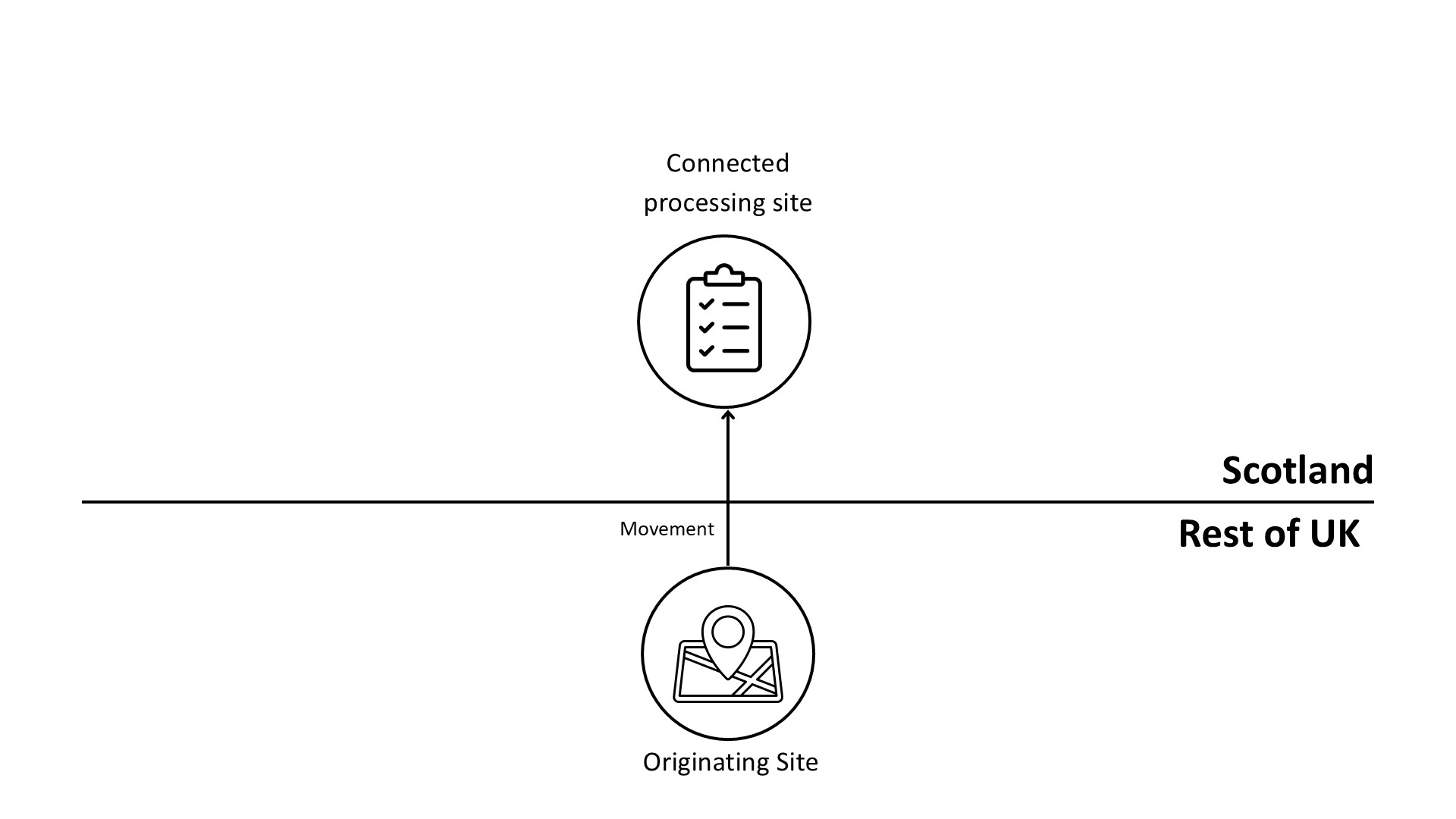

A quarry operator that owns a quarry site based in the rUK and a concrete plant based in Scotland transports crushed stone from the rUK quarry site to the concrete plant in Scotland.

Diagram 4 – movement of aggregate from rUK to a connected site in Scotland

The rUK quarry operator will be required to:

- register with Revenue Scotland and register with HMRC if they have not already done so

- make a return to Revenue Scotland detailing the Scottish Aggregates Tax due in relation to the aggregate – please see below regarding the timing of the Scottish Aggregates Tax charge.

The rUK quarry operator should also make a return to HMRC which includes a claim for a UK Aggregates Levy tax credit in relation to the supply of aggregate.

If the quarry operator registers both the rUK quarry site and the Scottish based concrete plant with Revenue Scotland, then there will be no Scottish Aggregates Tax due until the first point of commercial exploitation after the aggregate is moved to the concrete plant. In this example, the first point of commercial exploitation is likely to be when the crushed rock is mixed to make the concrete product.

If the quarry operator does not register the concrete plant with Revenue Scotland as a connected site, then Scottish Aggregates Tax will be due at the point when the aggregate is moved to Scotland.

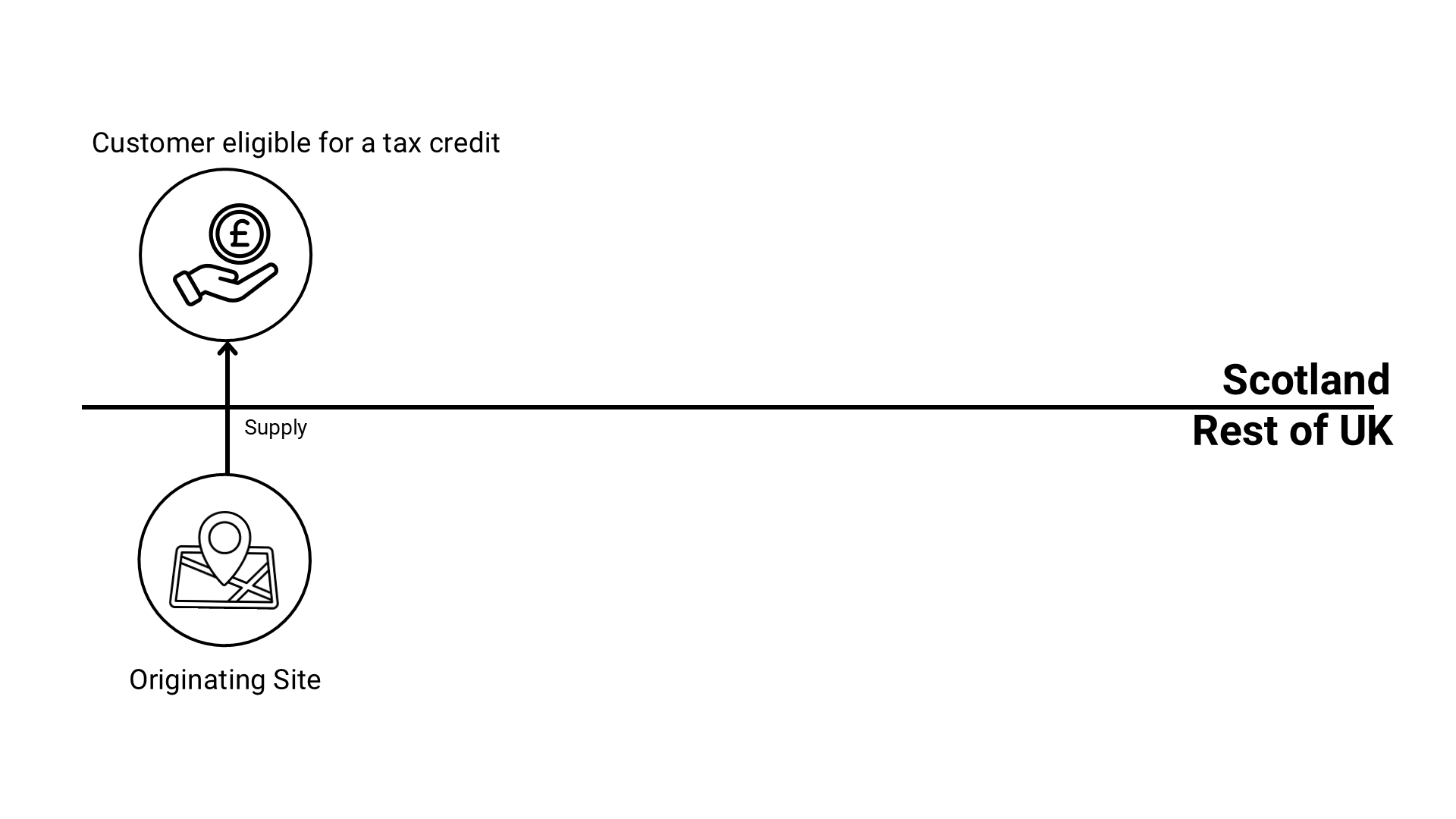

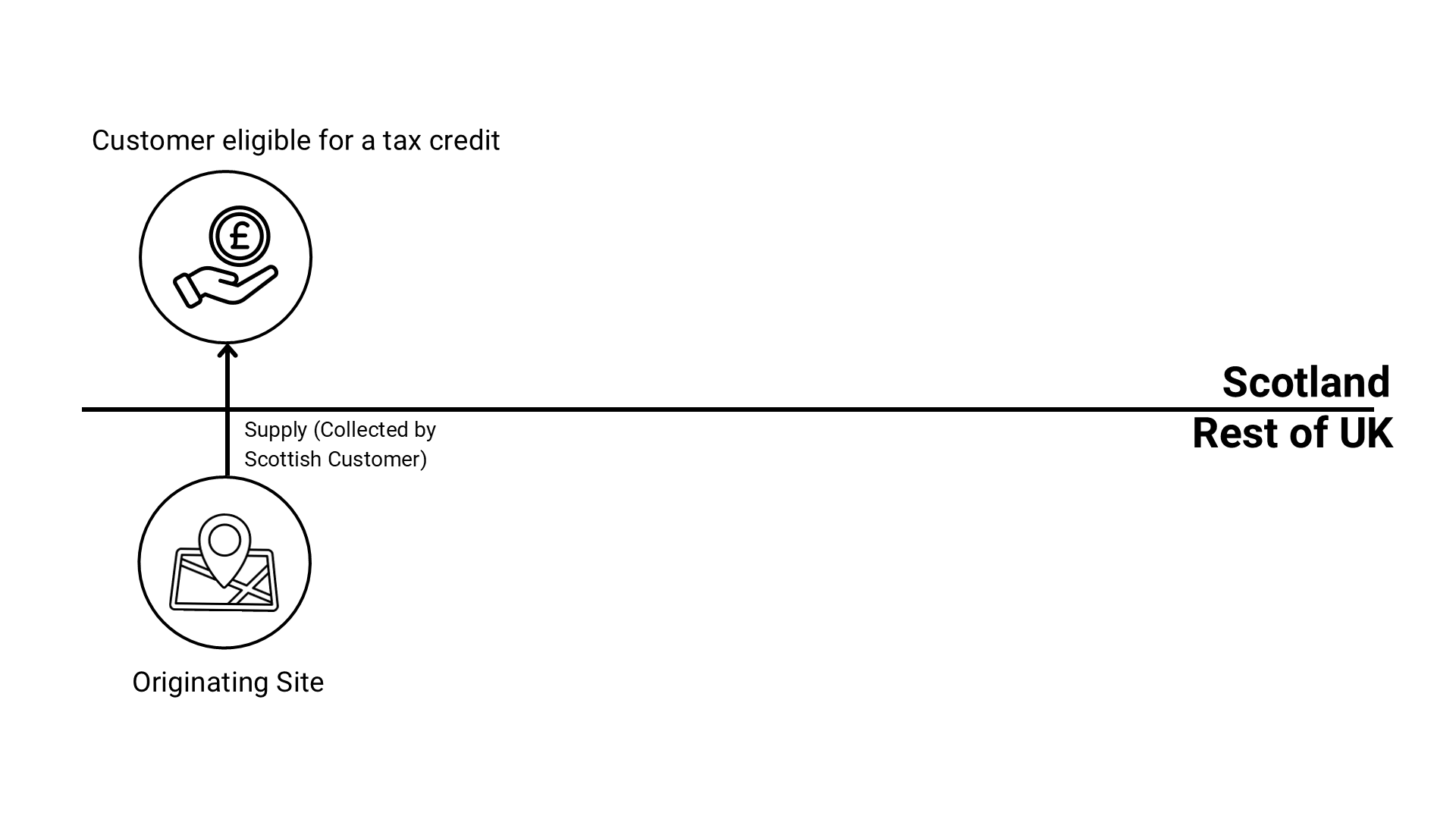

A quarry operator that owns a quarry site based in rUK may supply aggregate to a Scottish customer who is also carrying out an activity that allows for a tax credit (see tax credit guidance) to be claimed. For example the customer may carry out a prescribed industrial or agricultural activity (see industrial or agricultural tax credit guidance). The rUK quarry site may deliver the aggregate (Diagram 5) or the Scottish customer may collect the aggregate (Diagram 6).

Diagram 5 – supply of aggregate from rUK to a customer in Scotland who is carrying out activity eligible for a tax credit

Diagram 6 – collection of aggregate from an rUK site by a Scottish customer who is carrying out activity eligible for a tax credit

A tax credit will be available in relation to the movement of aggregate from rUK to Scotland and a tax credit will also be available for the activity being carried out by the Scottish customer. Care should be taken to ensure that the correct tax credit is being claimed, details of the expected approach for taxpayers are set out below but the underlying principal is that a cross border tax credit should be claimed whenever aggregate crosses the Scottish border.

The rUK quarry operator will be required to:

- register with Revenue Scotland and register with HMRC if they have not already done so

- make a return to HMRC which includes a claim for a UK Aggregates Levy tax credit in relation to the supply of aggregate across the Scottish border

- make a return to Revenue Scotland detailing the Scottish Aggregates Tax chargeable in relation to the aggregate and include a claim for the tax credit in relation to the eligible activity being carried out by the Scottish customer

If the Scottish customer is collecting the aggregate from the rUK quarry then the rUK quarry will first have to determine if the customer is delivering that aggregate to Scotland or somewhere else in the UK (see Example 2 – Collection from a rUK quarry by a Scottish customer for more details).

Aggregate moving from the rUK to Scotland – Indirect transfers

Aggregate that is moved from an rUK based supplier (typically a quarry) to a Scottish based customer through one or more rUK based intermediaries are described as ‘indirect transfers’ in this guidance. Transactions involving only an rUK based supplier and a Scottish based customer are referred to as ‘direct transfers’.

The general rule for cross border transactions is that if Scottish commercial exploitation occurs due to movement of aggregate from an rUK supplier to a Scottish based customer, then Scottish Aggregates Tax will be due on that transaction unless any relevant exemption applies. One such Scottish Aggregates Tax exemption is available where aggregate has already been charged to UK Aggregates Levy. This exemption may apply in indirect transfer scenarios as UK Aggregates Levy may have been paid by the original rest of the UK supplier when they supply aggregate to the rUK based intermediary. The intended outcome for onward sales from intermediaries in an indirect transfer scenario is therefore for that sale to be exempt from Scottish Aggregates Tax, providing UK Aggregates Levy has already been charged.

Whether Scottish based commercial exploitation has occurred will be a consideration at the last point in the supply chain to Scotland as this is the transaction where an rUK person may have supplied aggregate to a Scottish based customer. If Scottish commercial exploitation has occurred but an exemption to Scottish Aggregates Tax exists due to UK Aggregates Levy having been paid, then no Scottish Aggregates Tax will be due.

In the reverse position, where aggregate is supplied to an rUK based customer from a Scottish based quarry operator through one or more intermediary, Scottish Aggregates Tax will be due on the supply of aggregate from the Scottish quarry operator to the Scottish based intermediary. There may be an exemption from UK Aggregates Levy (please see the HMRC cross border guidance). This is a mirrored outcome for indirect transfers made to Scotland from an rUK based supplier, as set out in this guidance.

If you have any uncertainty with regards to how Scottish Aggregates Tax should be applied, then please contact SAT@revenue.scot.

If you have any uncertainty about how the UK Aggregates Levy should be applied, then please visit the HMRC website.

Diagram 7 - indirect supply from the r UK to Scotland, detailing the last point of the supply chain

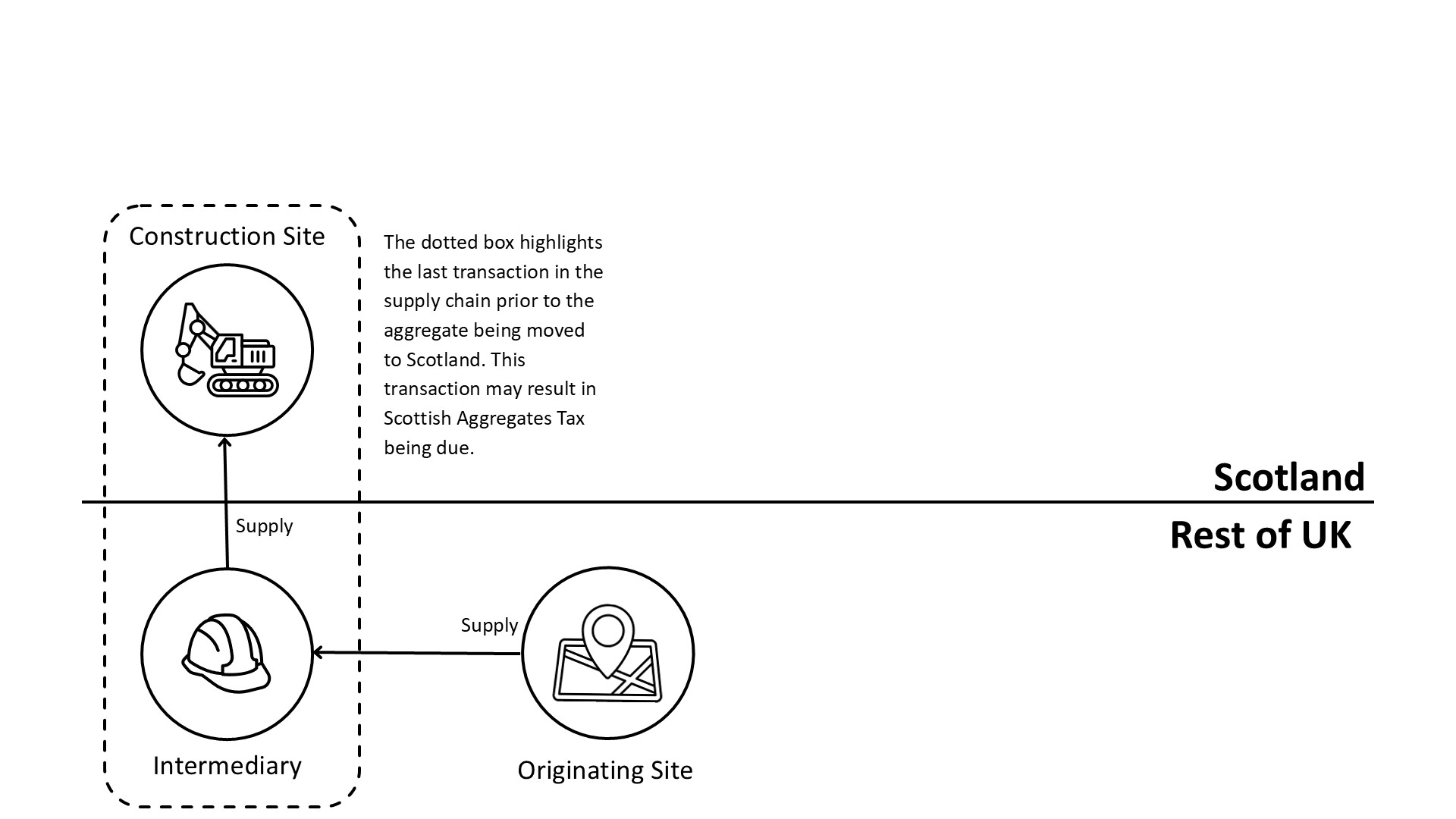

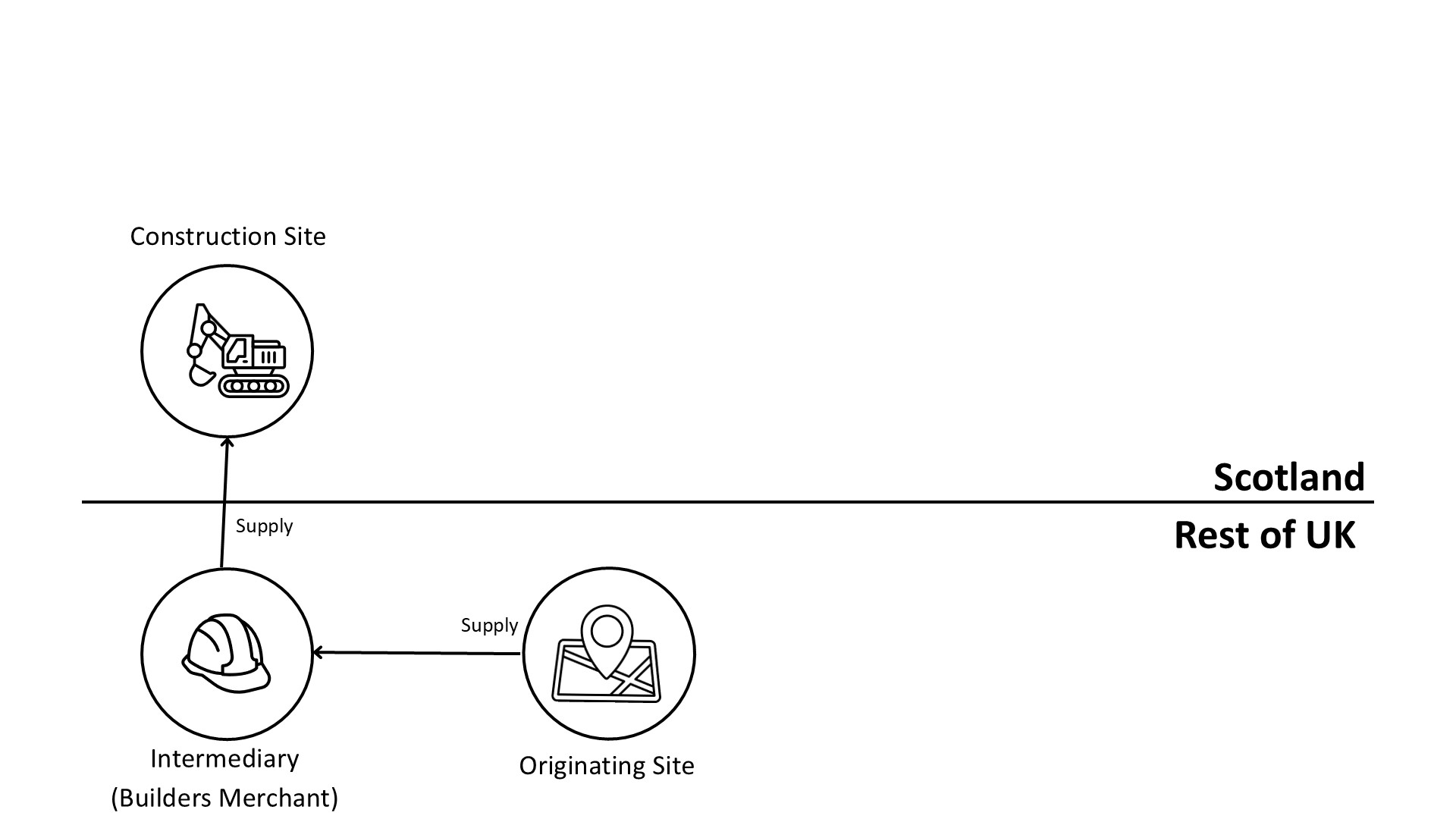

An rUK quarry operator sells gravel to an rUK intermediary (for example, builders’ merchants or bagging plants) who then sells and delivers the aggregate to a Scottish based customer.

Diagram 8 - indirect supply from the rUK to Scotland through an rUK intermediary

The rUK quarry operator will be required to:

- register with HMRC if they have not already done so

- make a return to HMRC to report and pay any UK Aggregates Levy due on the supply of aggregate to the rUK intermediary

The rUK intermediary and the Scottish customer will not be required to register for or pay Scottish Aggregates Tax as the original rUK supplier has already paid UK Aggregates Levy on that quantity of aggregate. The rUK intermediary would also be exempt from UK Aggregates Levy due to UK Aggregates Levy already being paid by the original rUK supplier (further details on UK Aggregates Levy exemptions can be found in HMRC guidance)

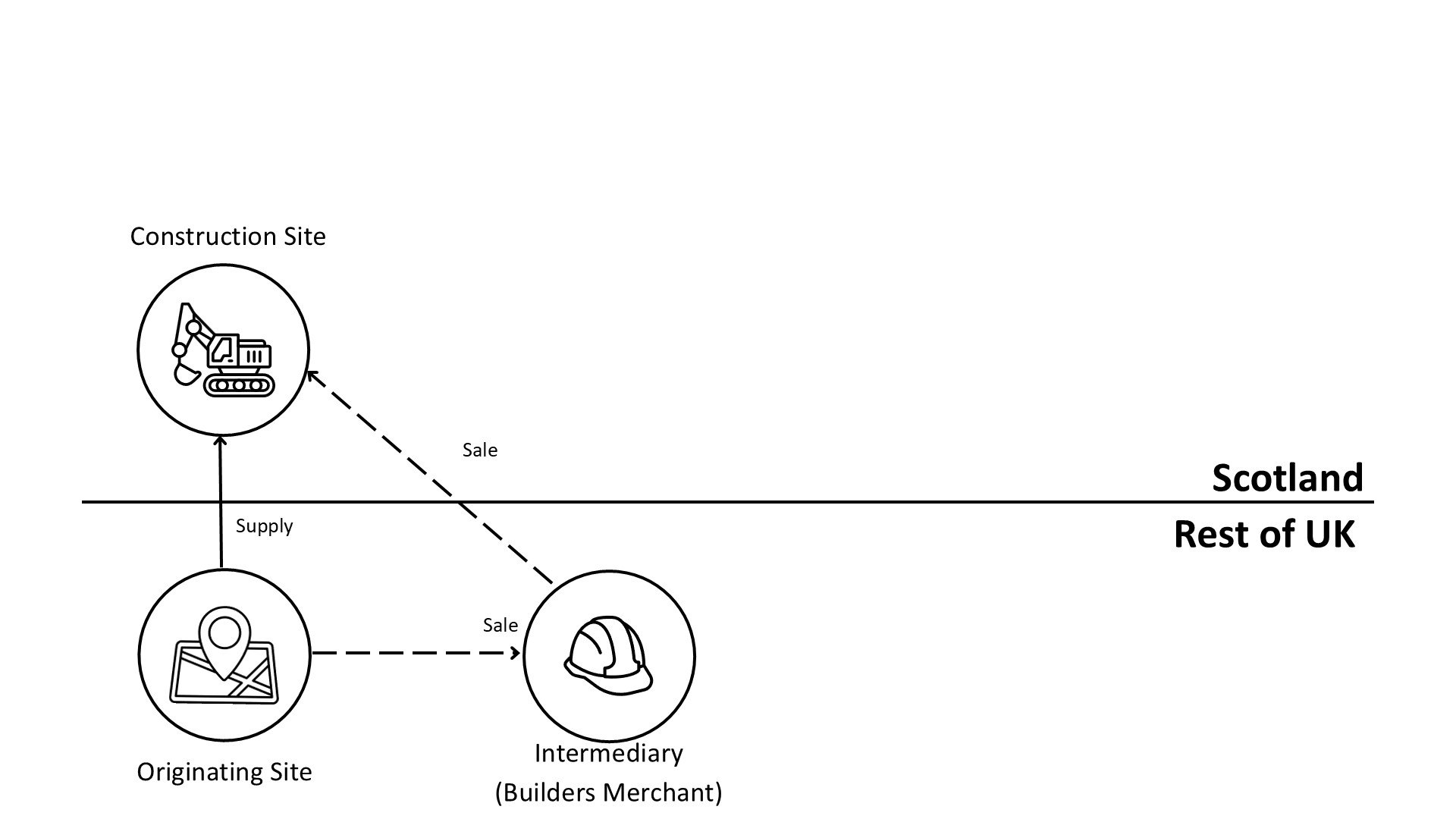

A builders’ merchant located in rUK has received a large order of aggregate from a Scottish based customer. The rUK intermediary does not have the required amount of aggregate stockpiled, so they ask an rUK based quarry to supply and deliver the aggregate to the Scottish customer on their behalf.

Although the original transaction is between the Scottish customer and the rUK builders’ merchant, the supply of aggregate is carried out by the rUK quarry. This supply is made directly from the rUK quarry to the Scottish customer and therefore the Scottish Aggregates Tax and UK Aggregates Levy obligations of the rUK quarry operator are the same as if the Scottish customer had made the purchase of aggregate directly from the rUK quarry. Full details for direct transfers.

Diagram 9 - indirect sale from the rUK to Scotland, supplied by an rUK quarry

The rUK quarry operator will be required to:

- register with Revenue Scotland and register with HMRC if they have not already done so

- make a return to HMRC which includes a claim for a UK Aggregates Levy tax credit in relation to the supply of aggregate

- make a return to Revenue Scotland detailing the Scottish Aggregates Tax due in relation to the aggregate

The Scottish customer will not be required to register or pay Scottish Aggregates Tax in respect of that supply as it has already been paid on the quantity of aggregate they have purchased.

The rUK builders’ merchant will not be required to register for or pay UK Aggregates Levy or Scottish Aggregates Tax in respect of that supply as the supply of aggregate in relation to both taxes has come from the rUK quarry site and the rUK quarry operator has accounted for both taxes.

Other scenarios

There may be other cross border scenarios that do not fit the categories of ‘direct’ or ‘indirect’ supply, as covered previously. The following guidance seeks to set out the main types of other scenarios that will be likely to occur in cross border transactions.

If you have any uncertainty with regards to how Scottish Aggregates should be applied, then please contact SAT@revenue.scot.

If you have any uncertainty about how the UK Aggregates Levy should be applied, then please refer to the HMRC guidance.

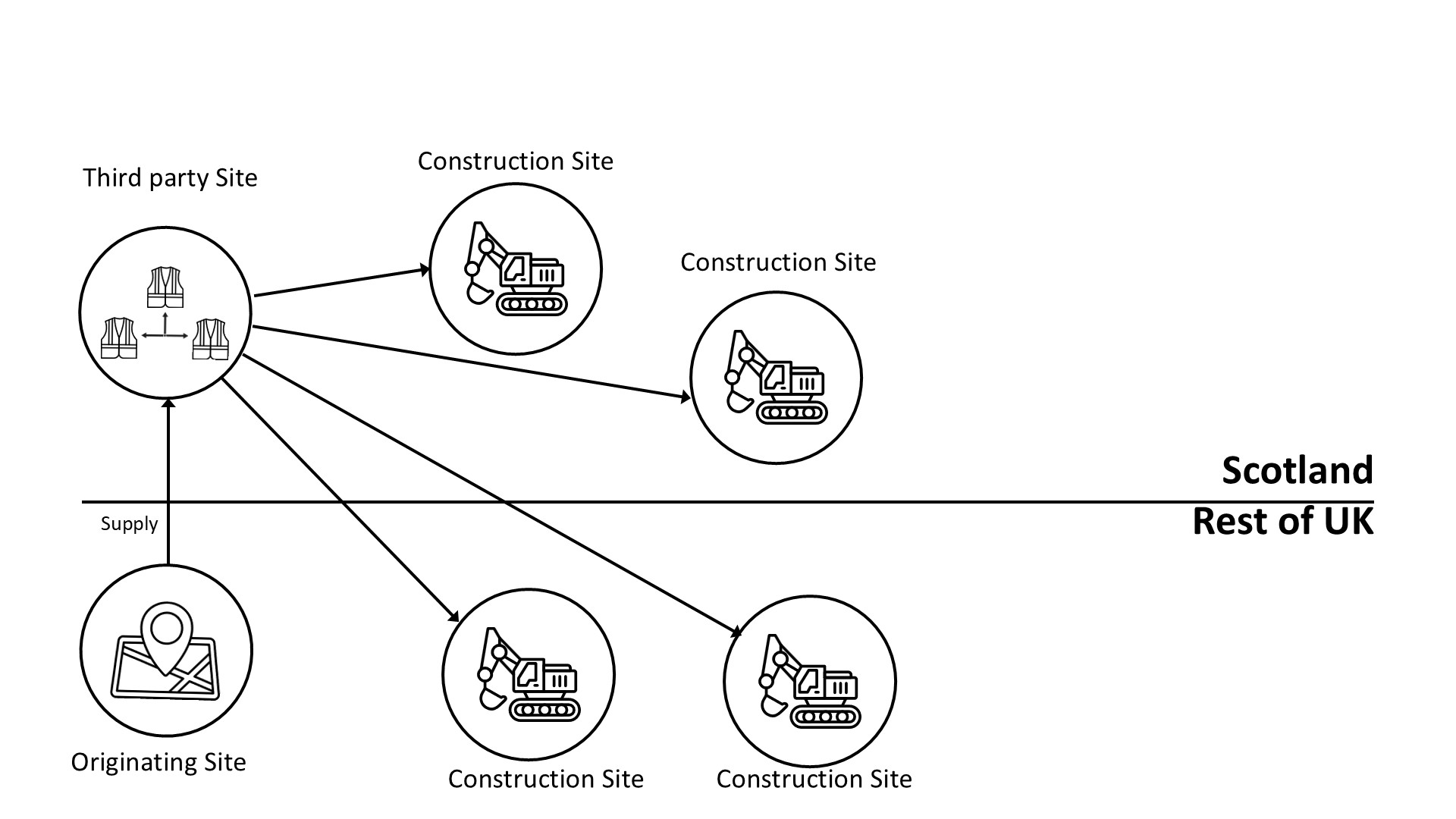

An rUK quarry supplies aggregate to a third-party depot located in Scotland. The Scottish based depot is part of a UK wide business, and it stores the aggregate until such time as it is needed. The depot may transport the aggregate to either a place in Scotland or a place in the rest of the UK, depending on where it is required at the time.

Diagram 10 – supply of aggregate back and forth across the Scotland / rUK border

The rUK quarry operator has undertaken a direct supply of aggregate to a Scottish customer and therefore the tax obligations of that operator are no different than what would be required in a basic direct supply scenario (see Example 1 - direct supply from rUK to Scotland).

The rUK quarry operator will be required to:

- register with Revenue Scotland and register with HMRC if they have not already done so

- make a return to HMRC which includes a claim for a UK Aggregates Levy tax credit in relation to the supply of aggregate

- make a return to Revenue Scotland detailing the Scottish Aggregates Tax due in relation to the aggregate

As Scottish Aggregates Tax has already been paid by the rUK quarry operator the Scottish depot will be exempt from the need to register or pay Scottish Aggregates Tax in respect of that supply when it supplies aggregate to Scottish based sites. The Scottish depot will also be exempt from UK Aggregates Levy when it supplies aggregate to the rUK based sites as there is an exemption from UK Aggregates Levy where Scottish Aggregates Tax has already been paid on a quantity of aggregate (HMRC cross border guidance). This exemption is equivalent to the one given for Scottish Aggregates Tax when UK Aggregates Levy has already been paid.

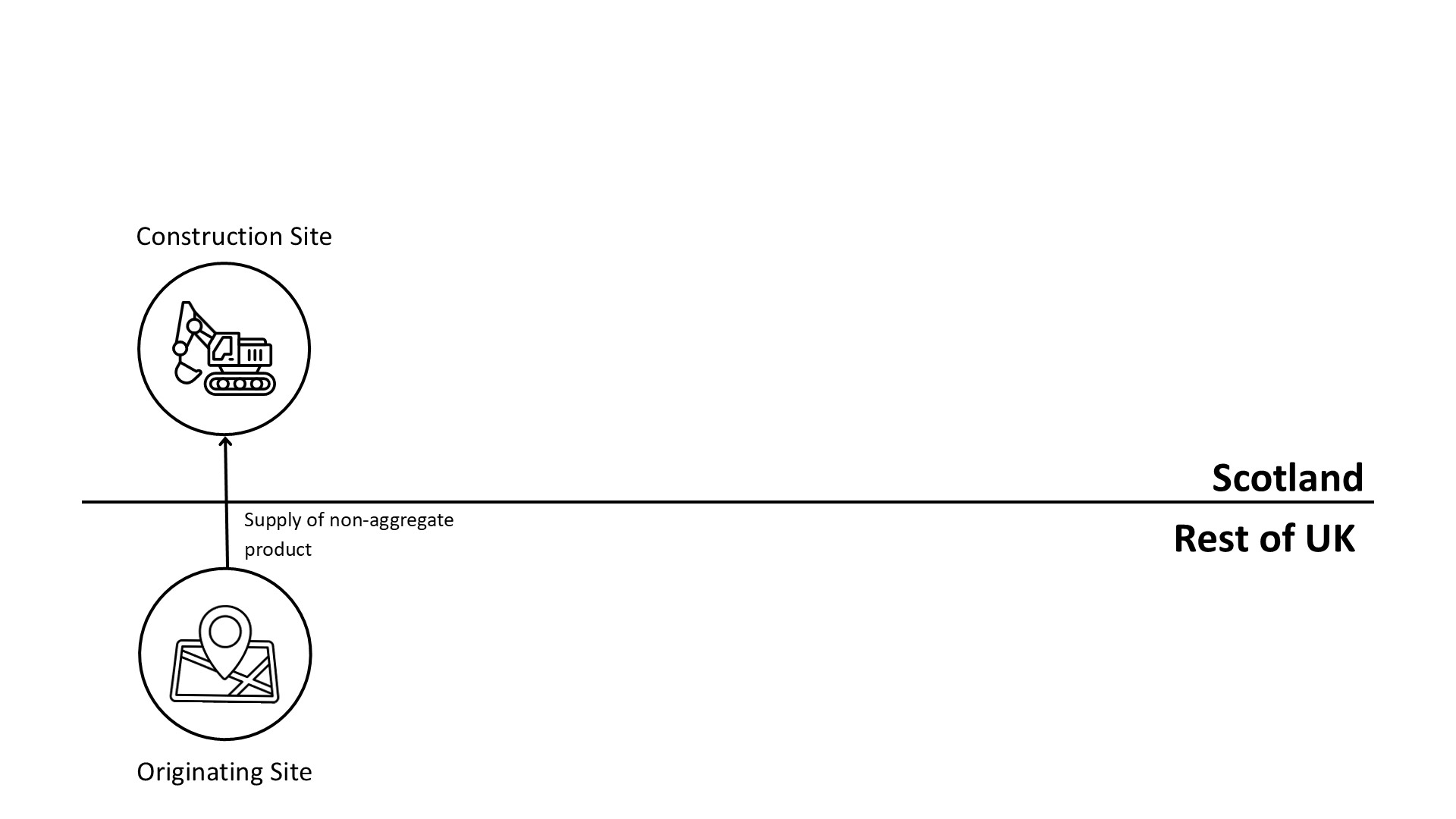

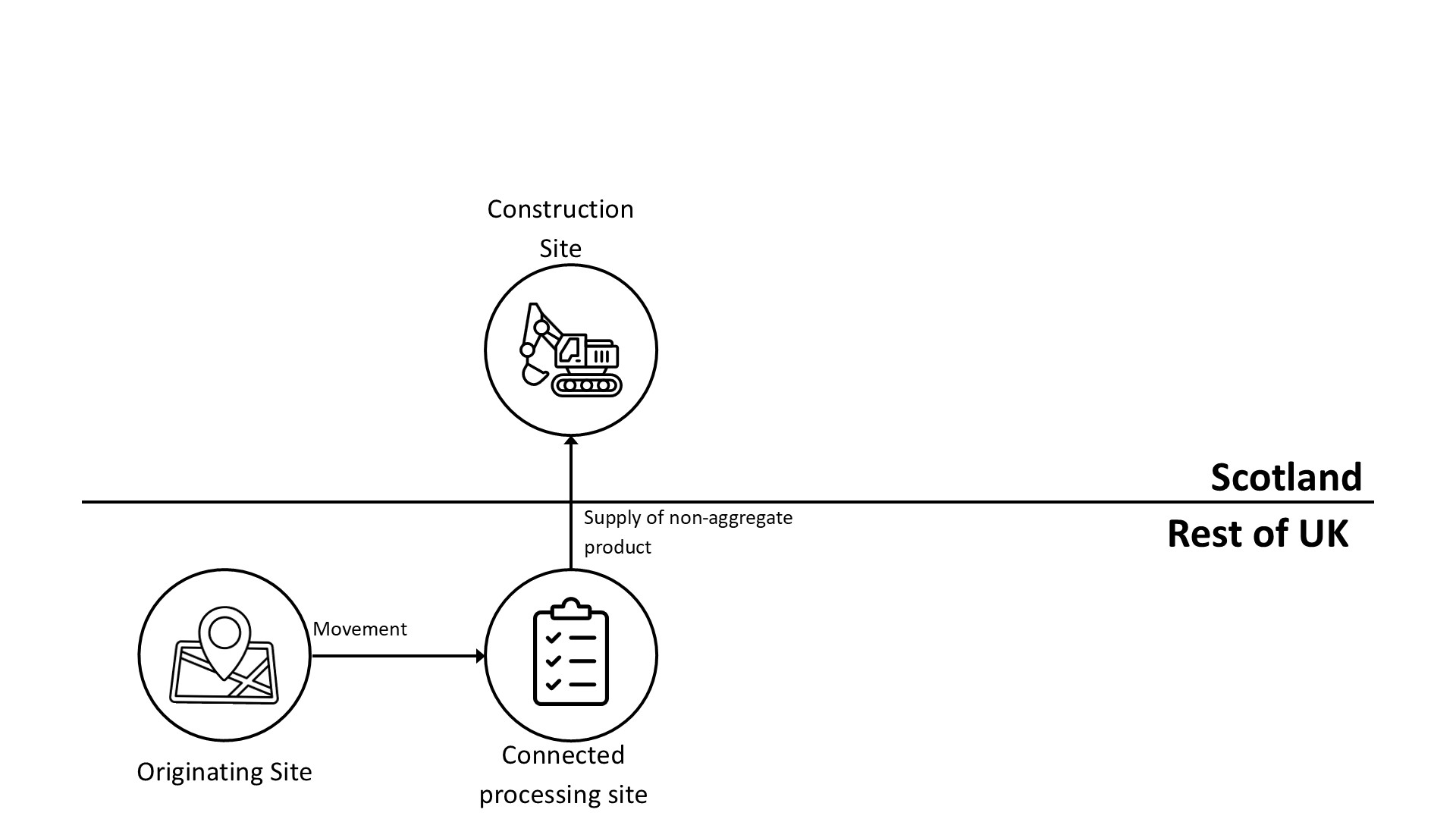

An rUK operator may either processes aggregate into another product (such as concrete or asphalt) on the same quarry site as they have won the aggregate from or transport aggregate to another connected rUK site for processing prior to supplying Scottish customers. If aggregate is processed into another product prior to supply, then this will not be considered a supply of aggregate for Scottish Aggregates Tax purposes as it is the processed product that has been supplied.

Diagram 11 – direct supply of a processed product from the rUK to Scotland

Diagram 12 – supply of a processed product from an rUK connected site to Scotland

In both cases there has been no supply of aggregate to Scotland as the aggregate has been processed into another product prior to the supply to a Scottish customer. As no aggregate has been shipped to Scotland, Scottish Aggregates Tax will not be chargeable. UK Aggregates Levy will however likely be due at the point at which the aggregate is processed into the new product. See the HMRC website for further guidance on when UK Aggregates Levy may be payable.

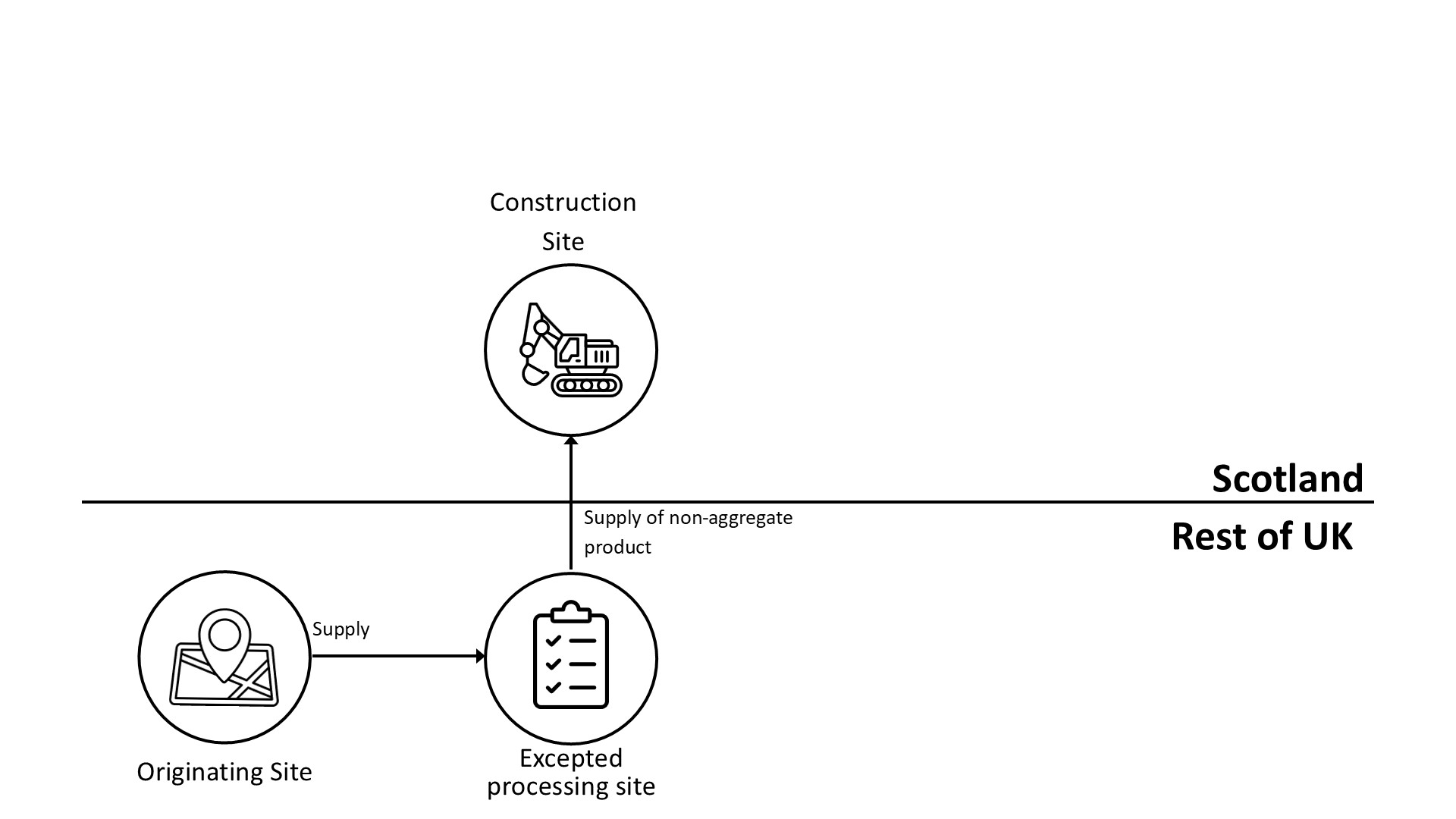

An rUK quarry operator may supply aggregate to another rUK site where the aggregate is used in an exempted process (creating dimension stone for example). Any products of the exempt process that are supplied to Scotland will not be considered aggregate for the purposes of Scottish Aggregates Tax. If waste or by-products from the process are supplied to Scotland then they may still be taxable.

Diagram 13 - excepted process being applied in the rUK prior to supply to Scotland

If the aggregate has been supplied for use in an exempt process, then the aggregate will be exempt from UK Aggregates Levy (see HMRC exempt process guidance for further details). As no material that is considered aggregate for the purposes of Scottish Aggregates Tax has been shipped to Scotland, Scottish Aggregates Tax will not be chargeable.

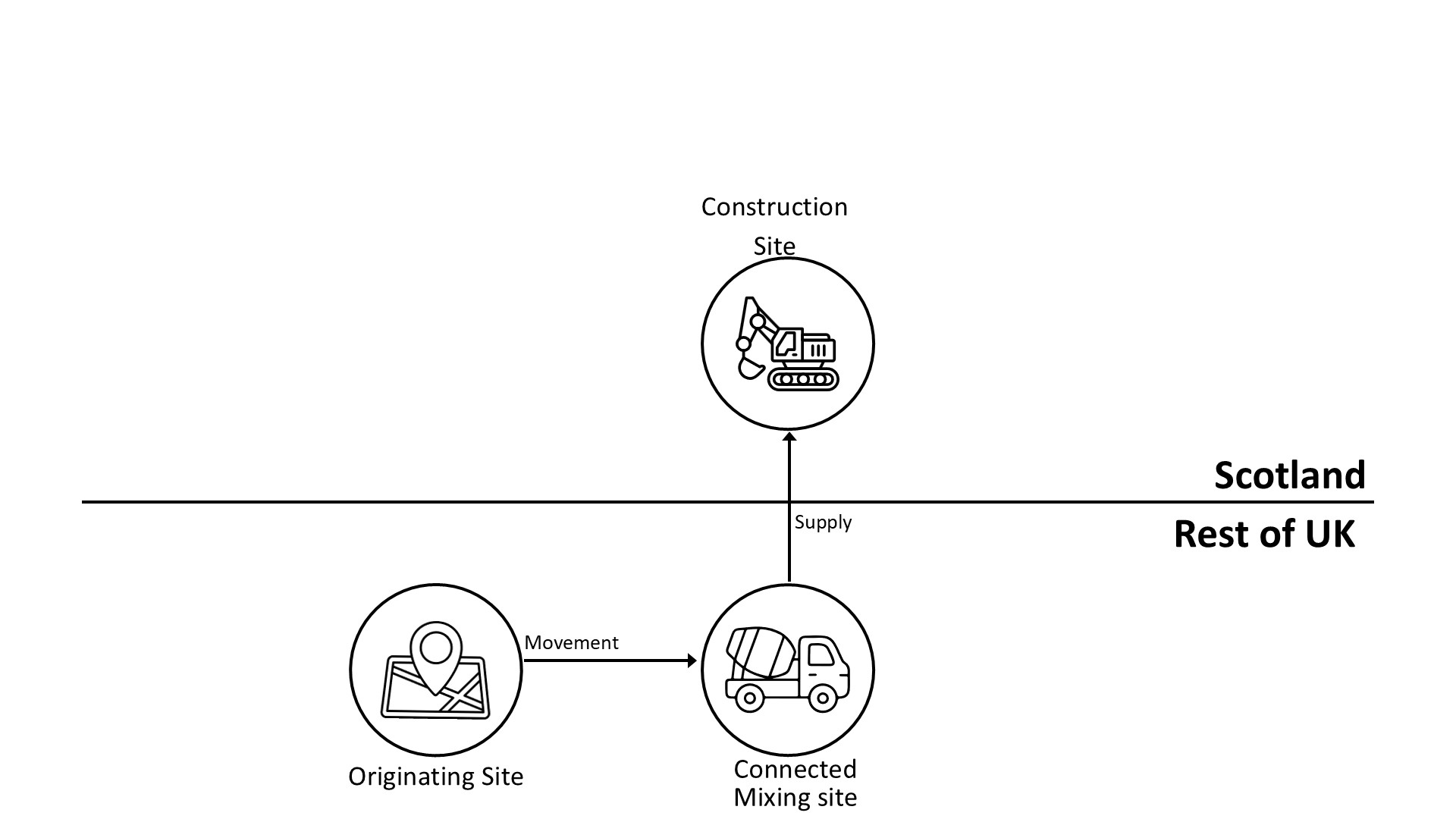

An rUK operator may either mix different types of primary aggregate together (to create ‘Type 1 aggregate’ for example) on the same quarry site as they have won the aggregate from or transport aggregate to another connected rUK site for mixing with other primary aggregate. If UK Aggregates Levy has not already been charged on any of the aggregate, then UK Aggregates Levy may not be chargeable at point of mixing - see HMRC guidance for further details.

Diagram 14 – direct supply of mixed aggregate to Scotland from the rUK

Diagram 15 – supply of mixed aggregate to Scotland from an rUK connected site

If UK Aggregates Levy has not been charged on the mixture of aggregate prior to supplying a Scottish customer, then the supply of aggregate will be chargeable to Scottish Aggregates Tax in the same way direct supply (see Direct Supply guidance).

The rest of the UK quarry operator will be required to:

- register with Revenue Scotland and register with HMRC if they have not already done so

- make a return to HMRC which includes a claim for a UK Aggregates Levy tax credit in relation to the supply of aggregate

- make a return to Revenue Scotland detailing the Scottish Aggregates Tax due in relation to the aggregate