About the Calculation

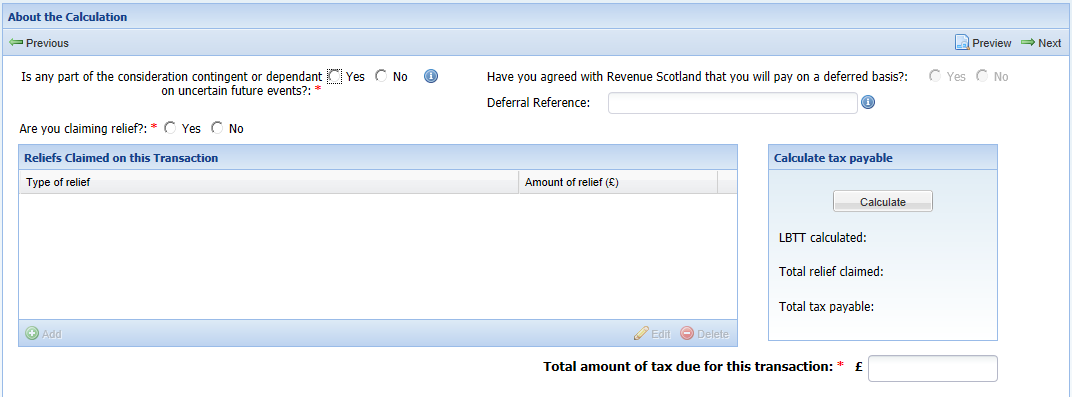

Is any part of the consideration contingent or dependent on uncertain future events?

You must answer this question. If you answer ‘Yes’ then you must also answer the later ‘Have you agreed with Revenue Scotland that you will pay on a deferred basis?’ question.

The payment of consideration, or an element of it, may be contingent or dependent on a future event, such as the granting of planning permission, or the final amount payable may be unknown until a future date.

Select ‘Yes’ if the transaction is subject to any events that could affect the transaction in the future as defined in sections 18 to 20 of the LBTT(S)A 2013 (contingent, uncertain or unascertained consideration – see LBTT2005).

Have you agreed with Revenue Scotland that you will pay on a deferred basis?

You must answer this question if you answered ‘Yes’ to the earlier ‘Is any part of the consideration contingent or dependent on uncertain future events?’ question. If you answered ‘No’ to that question then this question will be greyed out.

In certain circumstances we may allow a buyer to defer payment of tax. Select ‘Yes’ if we have agreed that you will pay some or all of the tax payable on the transaction on a deferred basis. See LBTT4016 for further guidance on applications to defer payment of tax.

If you have made an application to defer payment of tax, and either we have rejected that application or you are still waiting to hear from us, then answer ‘No’ to this question (but as outlined in the guidance for the later ‘Total amount of tax due for this transaction’ question, in the event of you waiting to hear from us about the application you can self-assess on the basis that tax will be deferred).

If a deferral application has been accepted by us and you are submitting a return or further return (under section 31 of the LBTT(S)A 2013) because the transaction has become notifiable or because tax or additional tax becomes payable as a result of a contingency ceasing or consideration becoming certain or ascertained (whichever applies), you should:

- answer ‘Yes’ to this question;

- state the deferral reference number we gave you when we accepted your deferral application in the ‘Deferral Reference’ question below; and

- enter the amount of tax that was deferred and is now payable in the ‘Total amount of tax due for this transaction’ question.

If a deferral application has been accepted by us, you have made an LBTT return and the result of a contingency ceasing or consideration becoming certain or ascertained (whichever applies) is that less tax is payable, you can claim a repayment of overpaid tax by amending the return if you are within time to do so (see the separate ‘How to amend an LBTT return’ for further guidance). If the time limit for amending the return has passed you may be able to claim under section 107 of The Revenue Scotland and Tax Powers Act 2014 for repayment of overpaid tax (see LBTT4021).

Deferral Reference

You must answer this question if you answered ‘Yes’ to the previous question.

If you have reached agreement with us regarding the deferral of a tax payment (see the question above), enter the deferral reference code that we gave to you.

Are you claiming relief?

You must answer this question.

Select ‘Yes’ if you are claiming one or more reliefs in relation to this transaction.

Reliefs claimed on this transaction

If you answered ‘Yes’ to the previous question then select ‘Add’ at the bottom of the ‘Relief claimed on this transaction’ box.

In the new window that appears after selecting ‘Add’, under ‘Type of relief’ select the relevant relief from the drop-down list and under ‘Amount of relief’ enter the monetary value of the relief that you are claiming.

Note:

- You can enter more than one relief for each transaction. It is your responsibility to ensure that you meet all the statutory requirements before claiming a relief. If you are uncertain about the application or conditions of a relief see LBTT3010 for further guidance.

- Neither a single claim of relief nor the total of two or more claims can be more than 100% of the total tax that is payable.

- If you are claiming charities relief you must answer both the ‘Charity Number’ and ‘Country’ questions in the ‘About the Buyer’ section of the return. This must be one of the permitted countries for charities relief – see LBTT3035 for further guidance on the conditions that must be met for charities relief. Charities relief cannot be claimed if the buyer is a charity which is not managed or controlled in one of the permitted countries for charities relief purposes.

Total amount of tax due for this transaction

Enter the total LBTT payable as calculated by you, rounded down to the nearest pound – ignore the pence. Note: This should not include any penalties and interest that may be due in relation to the transaction – these are administered separately by us.

To help you out you can select ‘Calculate’ in the ‘Calculate tax payable’ box which will display the total tax payable based on the information you have entered elsewhere in the LBTT return. Please note however that because LBTT is a self-assessed tax the buyer is ultimately responsible for the amount entered against this question. While we have provided the ‘calculate tax payable’ function for your assistance, we take no responsibility for your use of it in answering this question.

Additional guidance on the ‘Total amount of tax due for this transaction’ field:

- If you make a further return (note: this is not to be confused with an ‘amendment’ to a return already made) in relation to an earlier transaction, for example at the three yearly review of a lease, and the effect of making the further return is that less tax is now payable, as a negative amount cannot be entered in this field you must enter ‘0’ and make a claim for repayment to us under section 107 of The Revenue Scotland and Tax Powers Act 2014 (see RSTP7003). Interest will be paid on any repayment of overpaid tax from the date of original payment by the buyer (see RSTP4004).

- If, in relation to the three yearly review of a lease, you (the tenant, or a person acting on behalf of the tenant) are making a return under paragraph 10 of schedule 19 to the LBTT(S)A 2013 (see LBTT6015) and the result is that no additional tax is payable compared to the amount paid at the time the last return for the lease was made (perhaps because there has been no change in the rent), then enter ‘0’. If more tax is payable, only enter this additional amount.

- If, in relation to the assignation of a lease, you (the assignor, or a person acting on behalf of the assignor) are making a LBTT return under paragraph 11 of schedule 19 to the LBTT(S)A 2013 (see LBTT6017) and the result is that no additional tax is payable compared to the amount paid at the time the last return for the lease was made (perhaps because there has been no change in the rent), then enter ‘0’. If more tax is payable, only enter this additional amount.

- If we have accepted an application from you or the buyer to defer payment of tax because of contingent or uncertain consideration then enter the total amount of tax due for the transaction less the amount that is deferred.

- If you have made an application to defer payment of tax because of contingent or uncertain consideration but are still waiting to hear from us as to whether it has been approved or rejected, you can self-assess on the basis that tax will be deferred (in which case enter the total amount of tax due for the transaction less the amount that is deferred).

- If some or all of the consideration for the transaction is uncertain or unascertained because it depends on uncertain future events, and it either does not meet the conditions for deferral or we have refused your application for deferral or you have chosen not to make an application for deferral, then enter the total amount of tax due for the transaction on the basis of a reasonable estimate of the amount of consideration for the transaction.

- If some or all of the consideration for the transaction is contingent on an uncertain future event, and it either does not meet the conditions for deferral or we have refused your application for deferral or you have chosen not to make an application for deferral, then enter the total amount of tax due for the transaction on the assumption that the contingency will be resolved so that the consideration is payable or, as the case may be, does not cease to be payable.