The ‘About the calculation’ section will only become editable once the ‘About the transaction’ section has been completed.

Guidance on how to complete the ‘About the transaction’ section can be found at About the transaction.

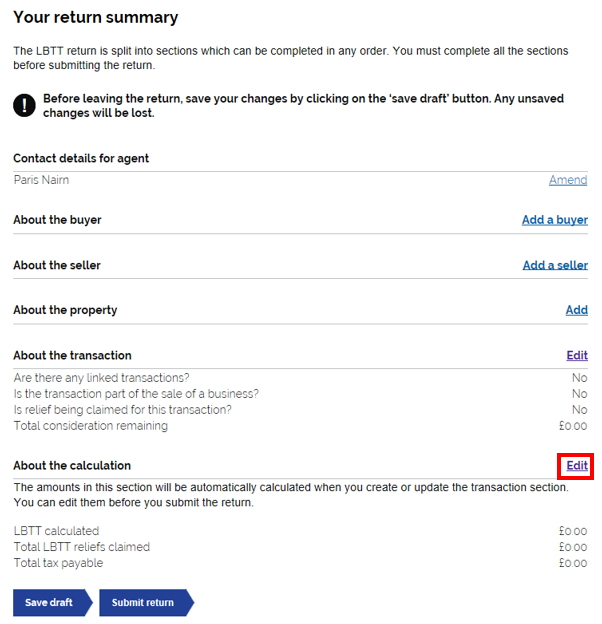

To edit, select the ‘edit’ button on the right of the ‘About the Calculation’ section. You will then be able to edit the following fields;

- LBTT Calculated – from the figure entered in ‘about the transaction’

- ADS Calculated – from the figure entered in ‘about the transaction’

- Totally liability – LBTT and/or ADS calculated

- Total LBTT reliefs claimed - from the figure entered in ‘about the transaction’

- Total ADS reliefs claimed - from the figure entered in ‘about the transaction’

- Total tax payable – Total liability minus LBTT and/or ADS reliefs claimed

Some of these fields may not be applicable to your transaction and will not need to be amended.

Note: These fields should not include any penalties and interest that may be due in relation to the transaction – these are administered separately by us.

Once you have amended the necessary fields, select next to update the changes. These will then be reflected on the Return summary area.