Revenue Scotland marks the introduction of the Scottish Aggregates Tax (SAT)

Revenue Scotland is pleased to confirm the introduction of Scottish Aggregates Tax (SAT), Scotland’s newest fully devolved tax, replacing the UK Aggregates Levy for all aggregate commercially exploited in Scotland. SAT comes into force following Scottish and UK Government legislation to switch-off the UK Aggregates Levy in Scotland and establish SAT.

Celebrating a decade of trusted administration: Highlights from our 10 year anniversary external events programme

As we mark ten years of delivering trusted, high quality tax administration, our anniversary year has provided the perfect opportunity to reflect with our partners and stakeholders on how far we’ve come - and to look ahead with renewed ambition. Over the past several months, we’ve hosted a programme of events designed to bring together partners, policymakers, experts and colleagues from across the public sector and beyond.

Driving better public outcomes through data, digital strategy and AI: Insights from Revenue Scotland’s anniversary webinar series

As part of Revenue Scotland’s 10th anniversary programme, two recent webinars brought together leading thinkers from across the UK and international public sectors – exploring how data, digital strategy, and AI can help organisations build trust, improve services, and operate with purpose and confidence.

Getting data right: Why quality, culture, and trust matter

Webinar held 19 February

Annex D: Key Terms

| Term | Definition |

|---|---|

| Consumer duty | A requirement for public bodies to consider how their policies and services affect consumers and ensure they are treated fairly. |

| Continuous improvement (CIMP) | An ongoing programme that delivers enhancements to systems and services—such as accessibility updates to SETS - to improve performance and user experience. |

| Declaration rates |

Annex C: Revenue Scotland People Survey - Equality and diversity

The Revenue Scotland People Survey asks if staff were discriminated against at work in the past 12 months and on what grounds. Due to small numbers, the detailed breakdown of discrimination responses has been suppressed to protect anonymity. The data is suppressed if less than 5% colleagues report experiencing discrimination.

Annex B: Gender pay gap

The gender pay gap is calculated as the difference between average hourly earnings (excluding overtime) of men and women as a proportion of average hourly earnings (excluding overtime) of men’s earnings. A positive pay gap means that men earn more than women on average, and a negative pay gap means that women earn more than men.

Annex A: Employee diversity data

The following charts show the composition of the Revenue Scotland staff body, broken down according to their protected characteristics. Data on Revenue Scotland staff is given for each of the previous three years.

The composition of Revenue Scotland staff is compared to data on Scotland's working age population. Comparator data on age and gender is taken from the National Records of Scotland’s 2024 mid-year population estimates for all people aged 16-65.

Consultation now live on modernising communications from Revenue Scotland

Scottish Government has today announced a consultation on modernising Revenue Scotland’s tax administration framework, specifically relating to communications from Revenue Scotland to taxpayers. You can view this consultation online here:

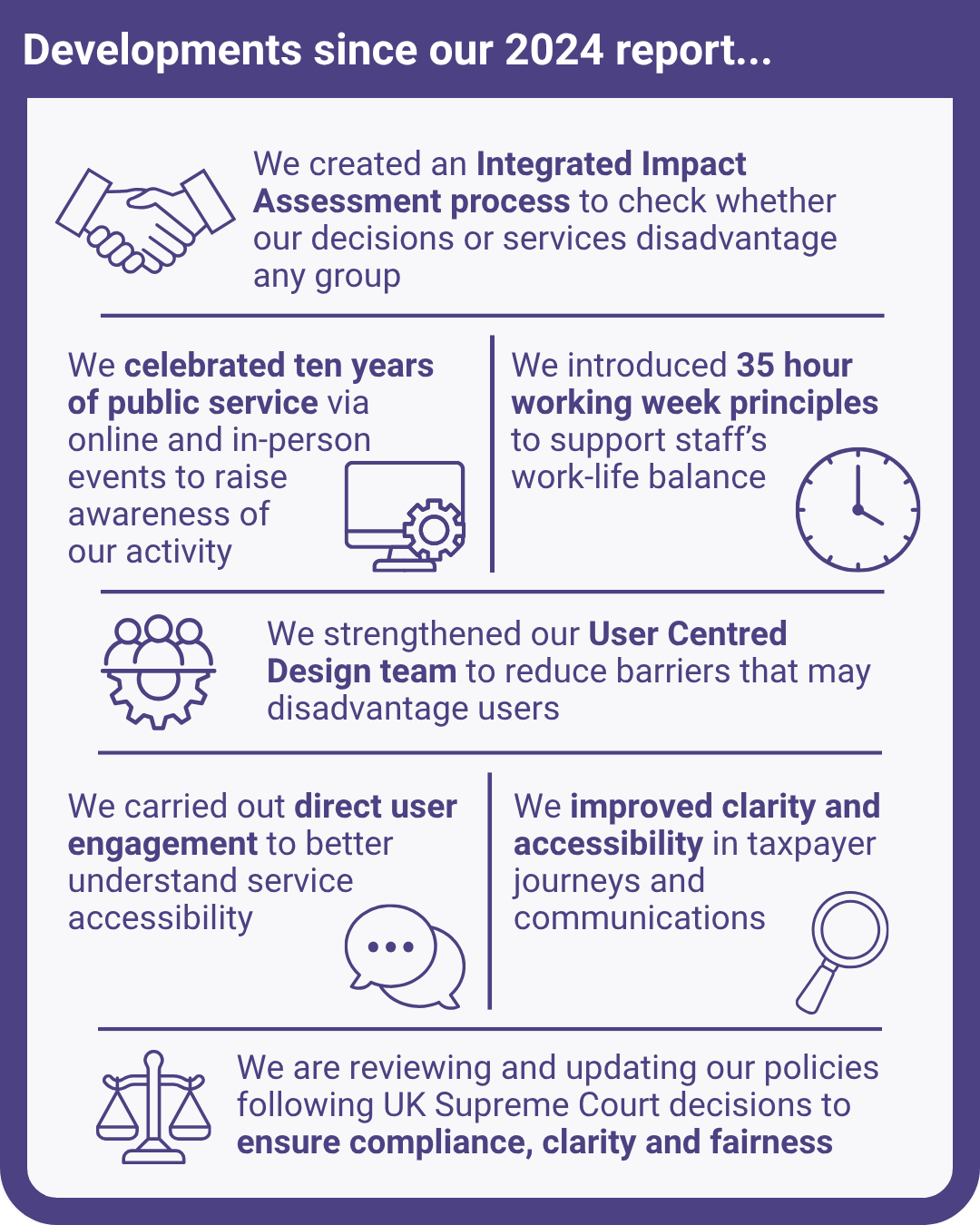

Developments since the Equalities Mainstreaming Report 2024

- We created an Integrated Impact Assessment process to check whether our decisions or services disadvantage any group

Gender pay gap

We provide at Annex B information regarding our gender pay gap and distribution between pay grades.